Currently yielding 5.1%, purchased shares of UPS (NYSE: UPS) would generate $6,550 in annual income if you invested $100k across both stocks. While there are question markets around the business and its full-year guidance, the stock still represents an excellent value for long-term investors. Here’s why.

A blue chip stock like UPS yields 5.1% for a reason, and that comes down to some market skepticism over the company’s dividend and/or its ability to grow its dividend. That’s understandable. After all, management’s stated aim is to pay about 50% of its adjusted earnings per share (EPS) in dividends. Unfortunately, with the market expecting just $7.49 in EPS this year, the current dividend of $6.52 is equivalent to 87% of its EPS.

Analysts asked management about the sustainability of the dividend on an earnings call earlier in the year, and CEO Carol Tome insisted, “We have no intent to cut the dividend just to make that math work.” In other words, the dividend won’t be cut so that UPS can meet its aim of paying a dividend equivalent to 50% of earnings. Instead, management plans to increase its earnings to get the ratio back to 50%.

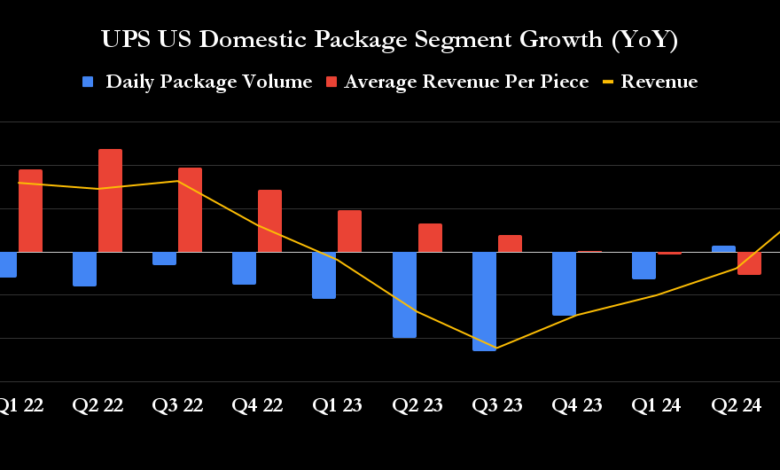

Fortunately, there is good reason to believe it can. After a couple of years of declining package volumes in its core U.S. domestic market, UPS is improving its volumes again, and its revenue is growing.

At the same time, the company is now lapping the increase in labor costs associated with a new contract agreed upon at the end of a protracted negotiation last year, making easier cost comparisons in the future. Moreover, UPS made good progress on costs in its domestic segment in the third quarter when reporting a 4.1% year-over-year decrease in cost per piece, which more than offset the 2.2% decline in revenue per piece , resulting in margin expansion.

Furthermore, UPS will reduce printing costs by $1 billion by cutting 12,000 jobs in 2024 as it reduces capacity to adjust to market demand.

As outlined in the Investor Day presentation in March, the U.S. small-package market moved from a capacity shortfall of an average daily volume of 6 million packages during the lockdown period to a capacity surplus of an average daily volume of 12 million packages in 2023/2024.

The overcapacity is due to an unexpected shortfall in delivery volumes due to persistently high interest rates slowing economic activity (there’s also the issue of customers shifting to lower-cost delivery options) and a spillover from the capacity increase made by the industry to deal with the capacity shortfall during the lockdowns.

https://media.zenfs.com/en/motleyfool.com/a1fcef1bd0b114d5cb4f1553bbc5e9cf

2024-12-23 03:06:00